Monday Signal Brief: Week of July 6, 2026

Affordability is showing up as a demand problem before a price problem. DARPI has retail asking prices holding while volume softens for a second straight week.

Here is what I am watching this week and what I would be doing about it at the desk.

The theme is affordability, and it is showing up as a demand problem before it shows up as a price problem. Our own DARPI read has retail asking prices holding while volume softens for a second straight week. The macro data explains why: buyers are stretched on payment, and the deal math is getting harder to structure. Five things worth your attention, then the numbers and the recalls that matter.

Payments hit $813 on the lowest June rate since 2022

Average June payment reached $813, a new June high, on an average APR of 6.7%, the lowest June rate since 2022 (J.D. Power). Incentives climbed to $3,217 per unit, around 6.2% of MSRP. And 29.5% of trade-ins came in underwater, up 1.4 points year over year.

A four-year low on rate that still lands on a record payment tells you the principal is the problem, not the APR. When principal is the problem, term is the wrong lever. It buys a lower payment by slowing equity build, and it does nothing for the near-30% of customers already walking in underwater.

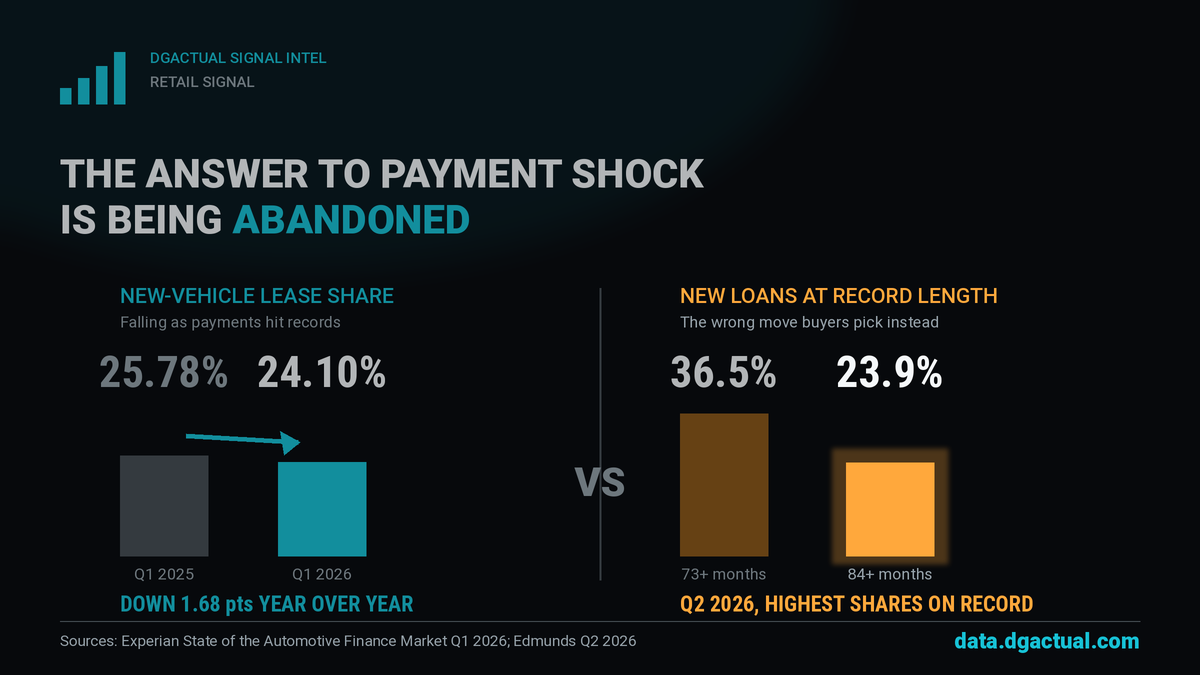

The lease is the tool built for this exact setup, and captive lenders will often buy a stretched customer at a better tier on a lease than they will on a long finance term, if they buy the long term at all. Put a lease payment next to every long-term loan quote this week and let the customer choose on the math.

A record one in four new buyers took an 84-month loan

Q2 2026 set a record: 23.9% of new-vehicle loans ran 84 months or longer (Edmunds). The average new-vehicle payment hit $777 on a record $44,156 financed, and 20.3% of new buyers are now carrying a payment over $1,000. Total interest on the average new loan works out to $9,811 at roughly 7.0% APR.

The 84-month term is not fixing affordability, it is deferring it. Buyers get a smaller payment by stretching principal over seven years, which means slower equity build and higher odds of coming back underwater at trade time. That is how negative equity compounds cycle over cycle.

Every 84-month deal you write is a customer who will not be equity-ready for four to five years. Build a re-marketing cadence that reaches them at year three with a data-backed equity check, and treat the lease as the alternative on the desk today, not the fallback.

3. The North America trade deal just got shakier, and it points to pricier cars later

Quick plain-English version. USMCA is the trade rulebook between the United States, Canada, and Mexico, the deal that replaced NAFTA. It is the reason a huge share of the cars and parts on your lot cross those borders with no tariff. Right now, a vehicle has to be about 75% North American-made to ship duty-free. On July 1 the administration chose not to lock the deal in for another 16 years. It does not expire, it stays in force through 2036, but instead of being settled it now gets reopened and argued over every single year. On top of that, there are already 25% tariffs on cars and parts coming from Canada and Mexico, and the push at the table is to make the rules tougher, raising that North American requirement toward 82% with a chunk required to be specifically US-made.

Here is what it means for your store, in one line: nothing to do today, but expect gradual upward pressure on both car prices and parts costs down the road. If more of a vehicle has to be built here to dodge a tariff, the cost of building it goes up, and that flows into window stickers and into the price of the parts your service lane buys. This is a slow-moving story, not a this-week story, so the play is simply to hold your service gross discipline now and not get caught flat-footed if parts costs start creeping. We will keep tracking it and flag it the moment it turns into something you actually need to price for.

4. Demand is contracting, but retail prices are not breaking

This is the DARPI read, and it is the most useful counterweight to the affordability headlines. Prices are holding. The softness is in volume and demand, covered in the DARPI section below. Do not confuse a demand-constrained market with a falling-price market. They call for different plays.

5. Three recalls with real service-lane opportunity

Over a million Jeeps under a park-outside warning, three-quarters of a million Ford and Lincoln units on a park-system defect, and a current-generation Hyundai Tucson do-not-drive campaign. Details and outreach angles in the recalls section. Each one is a reason to call a customer before they call you.

DARPI: prices are holding, buyers are not

Quick plain-English version: dealers are still asking full money for used cars, but fewer buyers are showing up to pay it. That gap between firm prices and softer traffic is the whole story this week, and it calls for a different playbook than a falling-price market would.

DARPI is DGActual's weekly index of what U.S. dealers are asking for used vehicles, built from more than 40 million active dealer listings plus private-party asking prices. It measures retail asking price, not the wholesale clearing price. Baseline 100 equals June 2026. Data as of July 5, 2026.

The one rule that matters: when demand is the constraint and price is not, you play for turn and for equity, not for sticker cuts.

- Late-model asking is essentially flat (DARPI Near-New 99.67, unchanged on the week versus 99.68 a week ago, just below the June 100 baseline). Late-model retail is not breaking.

- Older used cars firmed a touch (DARPI Value 98.82, up 0.17 points from 98.65). The higher-mileage cohort is holding, not sliding.

- Demand is what is cooling, not price. DARVI, our volume index, slipped 0.35% to 83.68, and the underlying demand score eased to 93.0 from 94.5. Both sit well under the 100 baseline. That is the softness hitting traffic and turn before it ever hits asking prices.

- The market signal is demand contraction for a second straight week. No single-week price or volume shock. This is a grind, not a break.

- Retail is holding its ground against wholesale (retail-versus-wholesale spread -0.33, roughly flat from -0.32). Sellers are not discounting retail to chase a softer wholesale line.

What it means for your store, in one line: manage days on market and turn, not sticker. A demand-constrained market rewards the store that stays disciplined on price and works the phones, not the one that pre-emptively cuts.

Segment detail worth acting on:

- Small cars are the one place late-model asking is strengthening. Midsize car near-new rose 0.52 points to 100.74 and compact car rose 0.40 to 100.17, both now above the 100 baseline. If you have that inventory, hold the line.

- Full-size trucks show the widest split by age. Late-model truck asking sits at 100.46, above baseline, while the older Value cohort is at 96.83, more than three points under. If you need to move metal, older trucks in the Value cohort are where you can discount without touching strong late-model truck gross.

- EVs split the same way. Late-model EV asking was the softest mover on the week, down 0.55 to 98.54. The older value-age EV cohort rose 0.48 to 101.74, the only segment holding a clear premium above baseline.

See the full brand and segment tables at data.dgactual.com/darpi.

The lease is the tool built for this market, and dealers are using it less

Quick plain-English version: buyers are stretched on payment and upside down on their trade. The one product on your lot designed to attack both problems at once is a lease, and lease share is falling right when it should be climbing.

A lease finances the depreciation, not the whole car, and it hands the depreciation risk back to the manufacturer instead of parking it on your customer's next trade. That is the mechanic. When a shopper is buying the payment down with term, the lease is the shorter road, not the longer one.

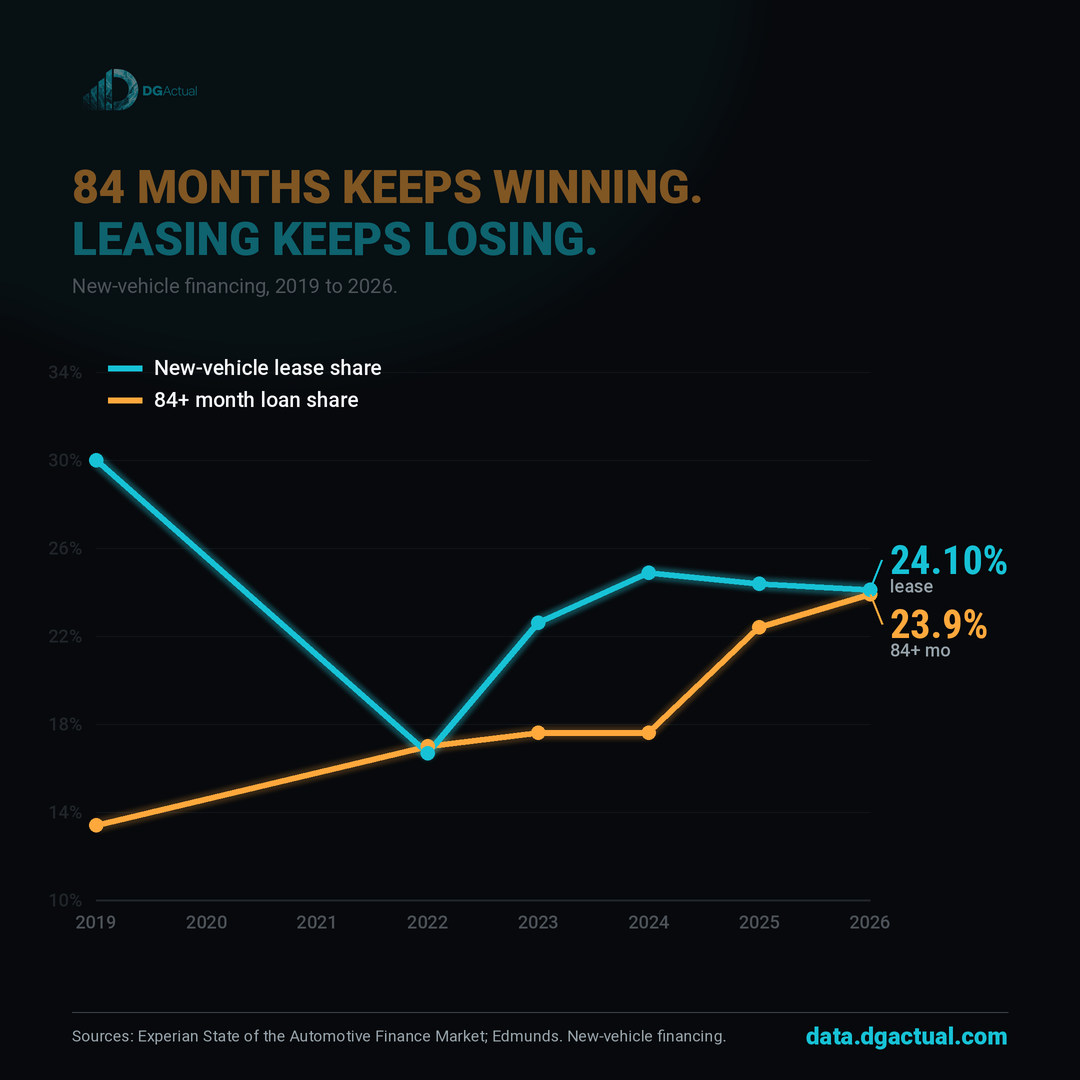

The numbers say buyers are choosing the opposite. New-vehicle lease penetration fell to 24.10% in Q1 2026, down from 25.78% a year earlier (Experian State of the Automotive Finance Market). Used-vehicle leasing is a rounding error at 0.26%. So at the exact moment affordability is the whole story, buyers are leasing less, not more.

Look at what they are choosing instead. A record 35.55% of new loans now run longer than six years, up from 30.83% a year ago, and a record 23.9% of Q2 buyers signed on for 84 months or longer (Edmunds). Nineteen percent of new-vehicle loans carry a payment over $1,000. Buyers are buying the payment down with term, which is the one move that deepens the equity hole they are already in.

The math is not subtle. The monthly payment gap between leasing and buying widened to $151 in Q1 2026 (Experian). On a payment-driven floor, $151 is the difference between a deal that pencils and one that walks.

There is a live proof point in the EV aisle. More than 56% of EV shoppers lease, and EVs now make up 25.31% of the total new-lease market, up from 17.69% a year ago (Experian). Where leasing is put to work on purpose, it dominates. The tool works. It is being used in one lane and ignored in the rest.

Two things a lease does that a long finance term cannot. First, it gives negative equity a finish line. Roll the underwater balance into the lease and it is paid off when the lease ends, instead of being carried forward into the next loan where it stacks on the new car's depreciation. Second, the approval math often favors the lease. Captive finance companies tend to buy a lease at a better tier than they will buy a prolonged finance term, if they approve the long term at all, so the same stretched customer can pencil on a lease that would have been declined or buried in rate on an 84-month note.

What it means for your store, in one line: put a lease payment next to every long-term loan quote, not just on the units with subvented money, and make the equity conversation explicit so an 84-month term reads as what it is, a slower road back to positive equity. When a buyer is stretched on payment and upside down on trade, leasing is not the fallback. It is the answer.

Recalls roundup

Three campaigns worth proactive outreach this week. All figures from NHTSA.

- Jeep Gladiator and Wrangler, model years 2021 to 2025, roughly 1,076,999 vehicles. An electrical connection in the electric hydraulic power steering pump wiring can overheat and potentially cause a fire, even when the vehicle is off. Owner notices begin July 9. This is a park-outside warning. Proactive outbound to schedule the remedy captures related service work, and clear safe-parking guidance protects the customer relationship. NHTSA release.

- Ford Explorer and Lincoln Aviator, plus Ford Expedition and Lincoln Navigator, model years 2018 to 2021 and 2020 to 2021, about 741,195 vehicles, campaign 26V402. A transmission valve-body separator plate may limit flow to the park valve, causing temporary park-pawl engagement while driving and potential damage that could allow unintended movement in Park. Owner notices begin August 3. The remedy is a software update plus transmission inspection and possible component replacement, which drives near-term appointments and parts and service-lane revenue. NHTSA Part 573.

- Hyundai Tucson, including Hybrid and Plug-In Hybrid, model years 2025 to 2026, 96,310 vehicles, campaign 26V400. This one is a do-not-drive. The instrument-panel display may reboot and go blank from a cluster and head-up-display software logic issue, potentially hiding the speedometer and warning telltales. Owner notices begin August 22. Service lanes can pre-book units that cannot take the update over the air for a dealer software fix, and use the visit to inspect battery and ADAS systems. NHTSA Part 573.

That is the week. Prices are holding, demand is the pressure point, and the deal structure is where affordability is landing. Play for turn and equity, not for sticker cuts.

Dealer-level ratings and market data live at reviews.dgactual.com and data.dgactual.com. Research support provided by AI tools; analysis and editorial by Daniel Govaer.