Signal Intel · May 26, 2026

3 min read · Signal Intel · May 26, 2026

Rates are stuck. Credit is stressed. Trucks just got a little tighter. You've got fresh intel and market to win. Good morning.

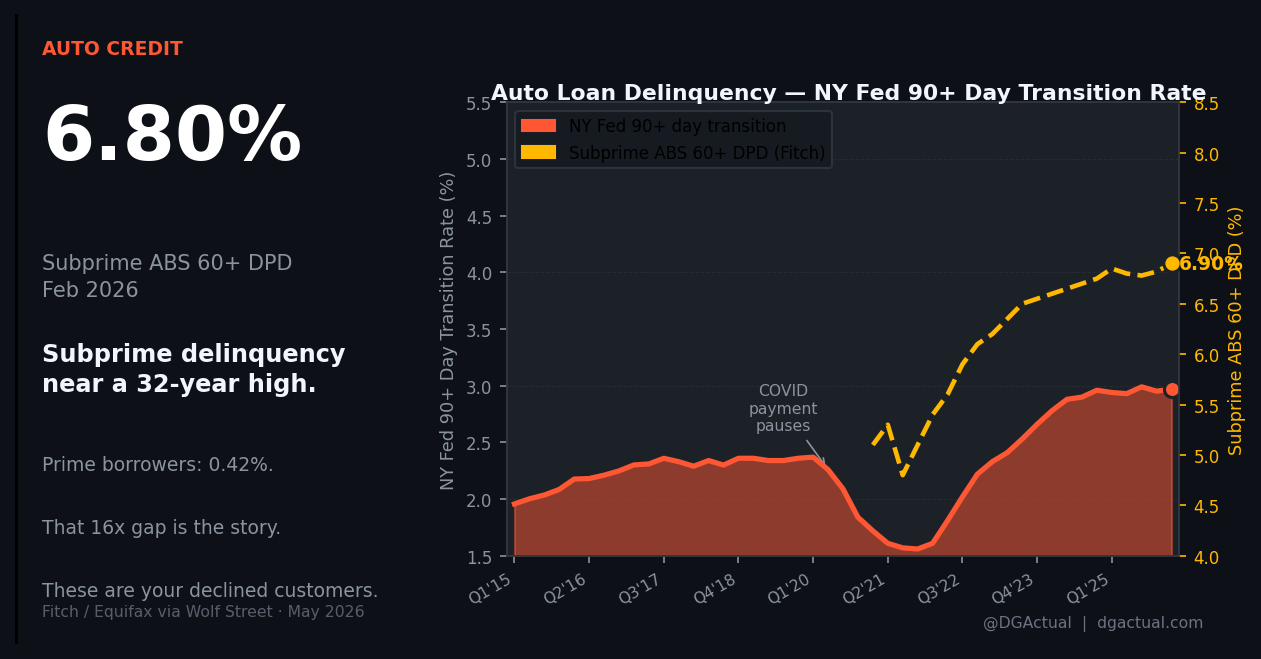

Subprime Is Bleeding Out Slowly

Subprime ABS 60-plus day delinquency hit 6.80% in February 2026, nearly 16 times the prime rate of 0.42%. That gap is the story. Prime borrowers are fine. Subprime borrowers are running out of runway, and the write-off data in the next signal confirms it.

When write-off accounts are up 26.8% year over year, the lenders are already running the math on their portfolio. According to Equifax's May 2026 Automotive Insights report, captive finance portfolios, where the majority of leases live, carry a 60+ day delinquency rate of just 1.1%. The lease is not just better for the customer's equity position. It is demonstrably safer paper.

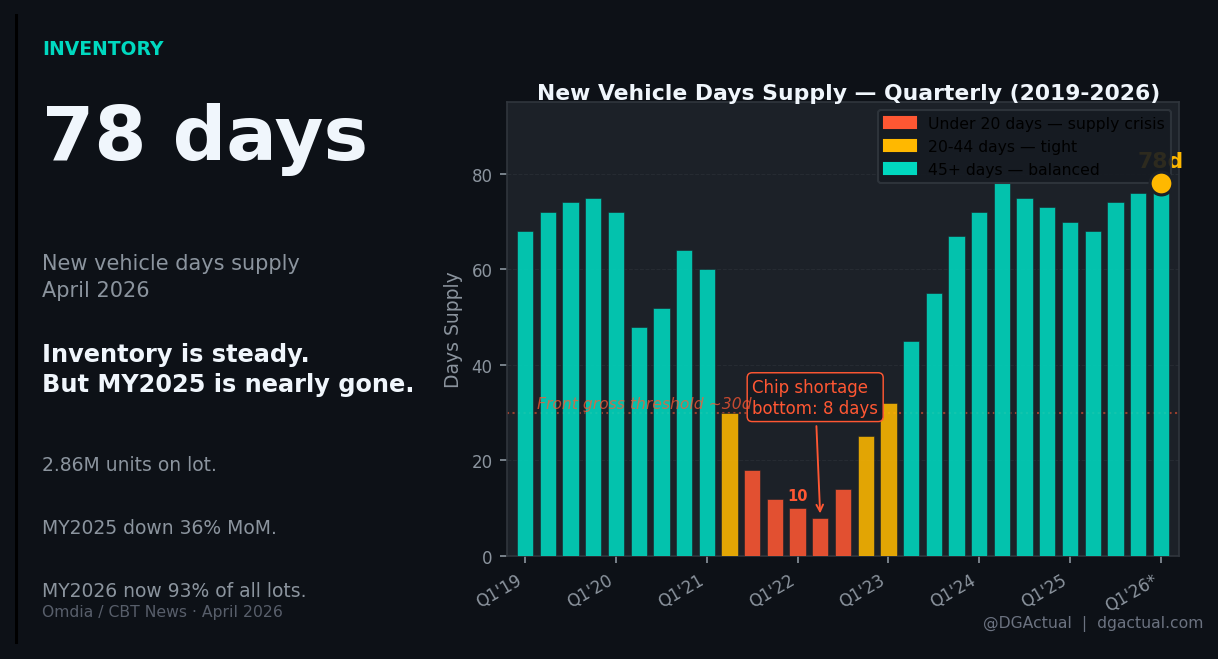

Inventory Is Stable, For Now

There are 2.86 million new units sitting on lots right now, averaging 78 days supply nationally. MY2025 inventory dropped 36% month over month as dealers cleared aging stock, and MY2026 now represents 93% of what's on the ground. Incentives are running at 6.9% of ATP, which means OEMs are still paying to move metal.

Seventy-eight days is a comfortable number, but it is a national average. If your mix skews toward a nameplate getting hit by tariffs or production issues, your local reality may look very different.

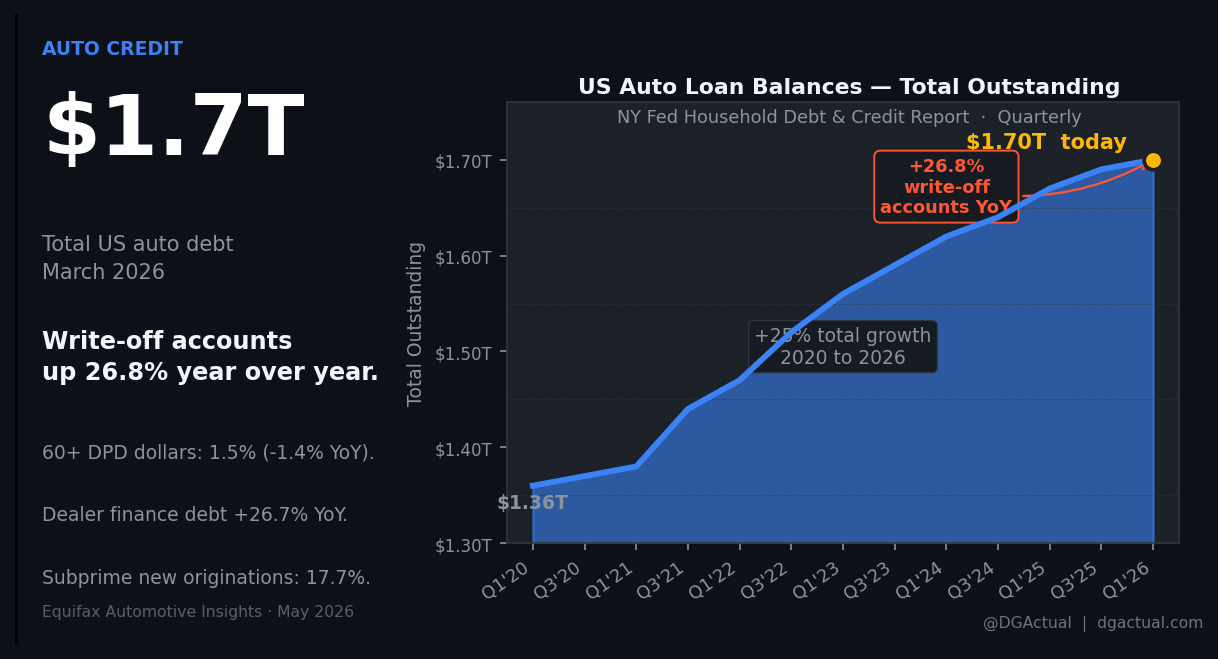

$1.7 Trillion and Counting

Total outstanding US auto debt crossed $1.7 trillion in March 2026, up 1.7% year over year. The headline number sounds fine. Look underneath: write-off accounts are up 26.8% year over year, and dealer finance debt specifically is up 26.7%. Subprime accounts for 17.7% of new originations year-to-date.

The 60-plus DPD dollar figure actually fell slightly, which sounds like good news until you realize write-off volume means more accounts are being charged off before they ever age that far. The problem is not slow. It is just ahead of the visible data.

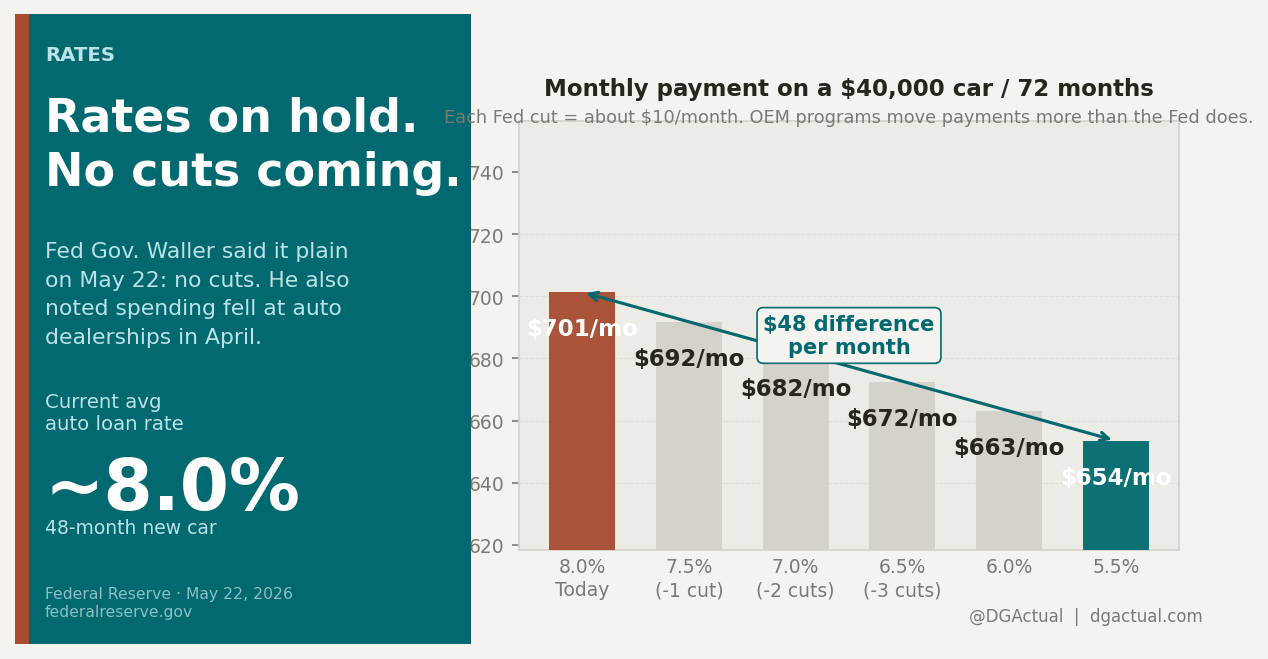

Waller Said No, and He Meant It

Fed Governor Waller spoke on May 22 and made it clear: no cuts are coming. He specifically called out a spending decline at auto dealerships in April. The average 48-month auto loan rate is sitting around 8%, and every Fed cut would only move the needle about $10 a month on a $40,000, 72-month note.

Stop building your sales floor's pitch around the Fed. OEM subvented rates move payments 30 to 60 dollars a month when the program is strong. That is your lever. Rate watch is a distraction.

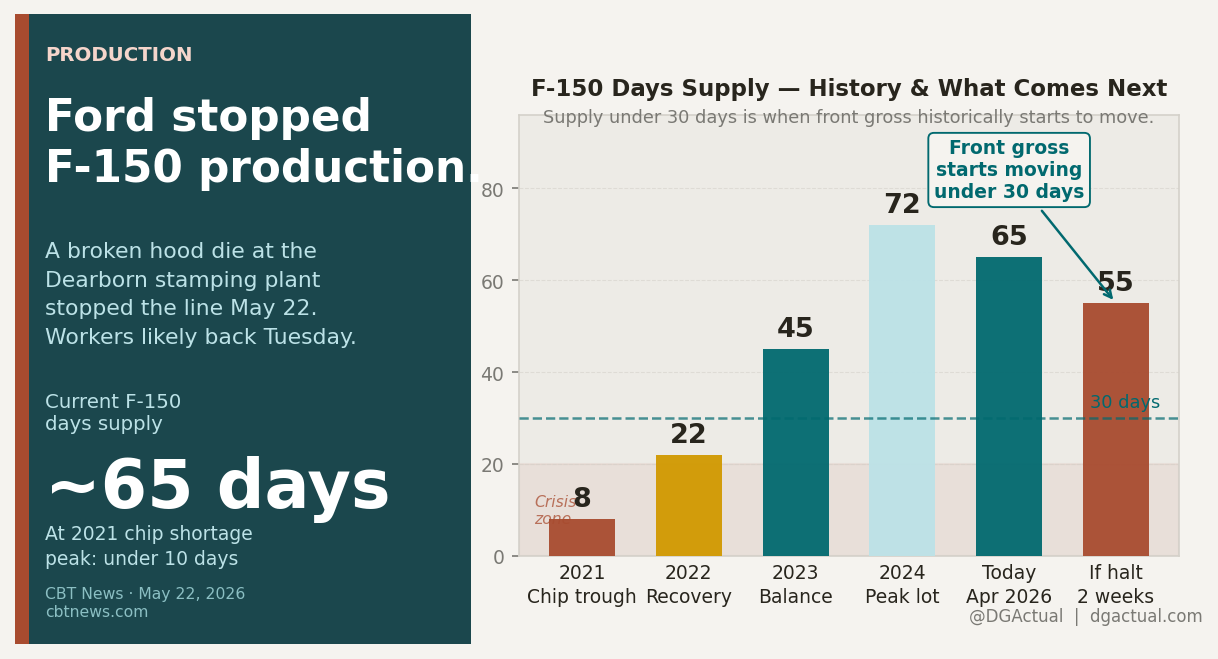

Ford Stopped Stamping F-150s

A broken hood die at Ford's Dearborn stamping plant shut down F-150 production on May 22. Workers were expected back Tuesday. Current F-150 days supply sits around 65 days nationally, well above the 30-day threshold where front gross historically starts to firm up.

Sixty-five days gives you cushion, but if the halt runs longer than a few days and regional stock gets thin, you could see a genuine scarcity moment on a unit that anchors a lot of back gross structures. Watch your appraisal desk closely. Trade values on competitive trucks will move fast.

Also Worth Knowing

Stellantis dropped its FaSTLAne 2030 plan last week: EUR 60 billion over five years, with 70% flowing to Jeep, Ram, Peugeot, and Fiat. Belvidere reopens in 2027, and the company officially walked away from 2030 EV mandates. Q1 2026 came in at a EUR 377 million profit against a EUR 387 million loss the prior year. Separately, NHTSA issued recall 26V316 covering 421,078 Hyundai vehicles: a front camera software defect that can trigger unexpected braking. There are 376 consumer reports on file and 4 confirmed crashes. The fix is a software update, and owner letters go out July 17.

The three real stories this week are connected. You have 17.7% of new originations going to subprime borrowers who are already delinquent at nearly 7% on existing paper. You have a rate environment that will not budge and a Fed official who just told you so directly. And you have a national inventory picture that looks stable until one supply chain event, like a broken die in Dearborn, reminds you how thin the margin for error actually is. The dealers who are going to hold gross through the rest of 2026 are not the ones waiting for conditions to improve. They are the ones who already know their closing ratio by credit tier, their VSC penetration by lender, and their service absorption well enough that variable ops is not the only thing keeping the lights on.

Daniel Govaer | EVP Product VINCUE | Loyalty Project Manager Beaver Toyota | Dealer Innovation Group Facilitator MyKaarma | Former Award-Winning Mercedes-Benz General Manager | NADA Academy Class N367 Graduate