Signal Intel · June 2, 2026

Loan terms stretch to 35.55%. Payment wall hits 1 in 5 buyers. Used prices up $870 in a month. 419K Jeep recall hits service lanes June 11. Credit splits into two markets.

3 min read · Signal Intel · June 2, 2026

Loan terms are stretching. The payment wall is mainstream. Used prices moved hard in a single month. A 419K-unit Jeep recall hits service lanes mid-June. Credit is polarizing. Five signals, one direction: the market is under pressure from both ends at once, and the dealers managing it well are the ones reading the math ahead of the floor.

** PS: The most complete (and entertaining) FTC analysis will be hitting your inbox tomorrow**

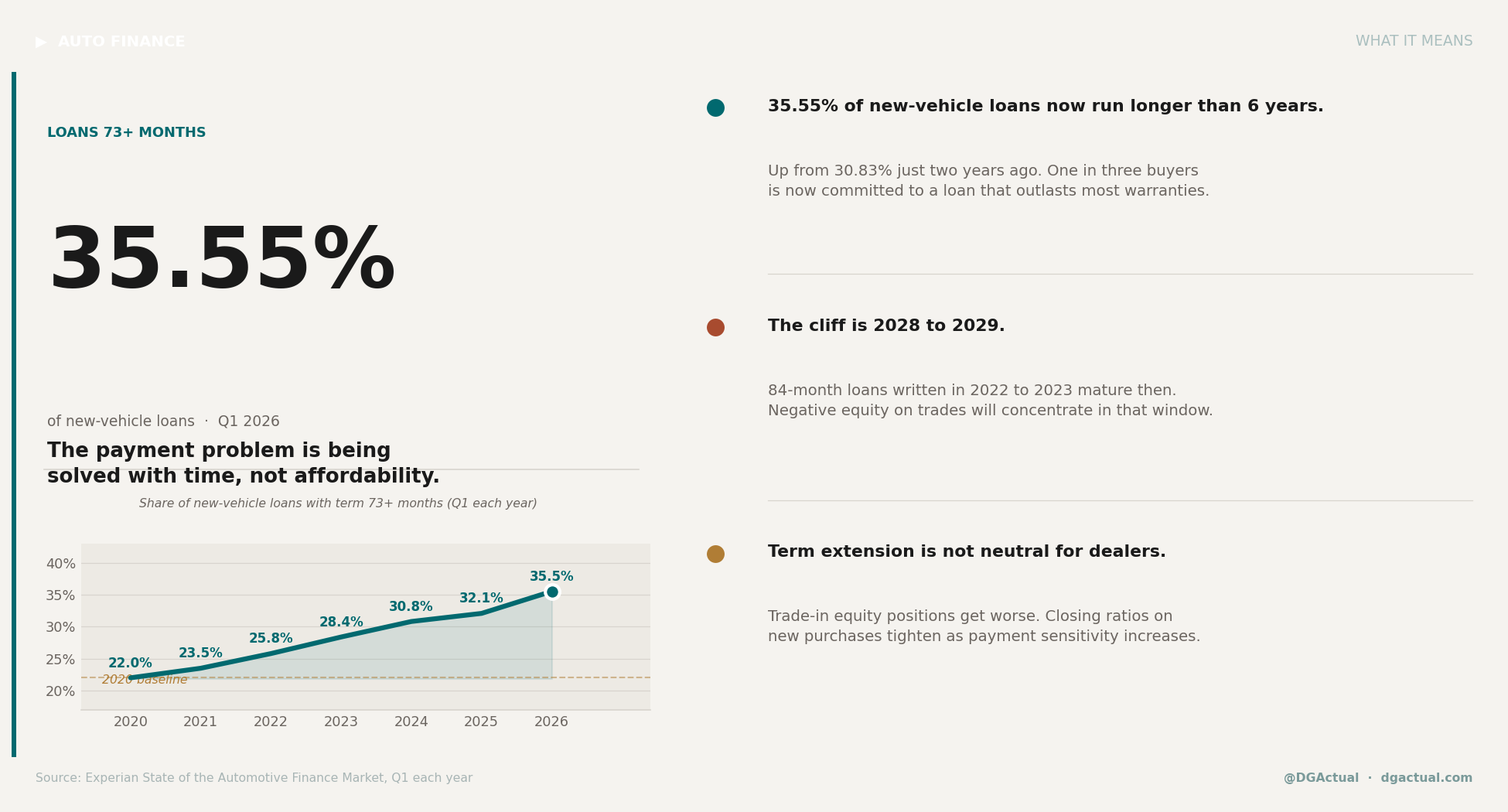

The Loan Is Now Longer Than the Warranty

35.55% of new-vehicle loans in Q1 2026 carry terms longer than six years. A year ago that number was 30.83%. One in three buyers is now committing to a loan that outlasts most factory warranties on the car they're buying.

Average new-car monthly payment: $770. Average amount financed: $43,925. Subprime's share of total auto financing: 15.75%, up from 14.40% a year ago.

The payment problem isn't being solved. It's being deferred. Every 84-month loan written today is a trade-in conversation that gets harder in 2028 and 2029, when those loans hit their maturity window with negative equity still baked in. The appraisal desk and the F&I office need to be running the same math.

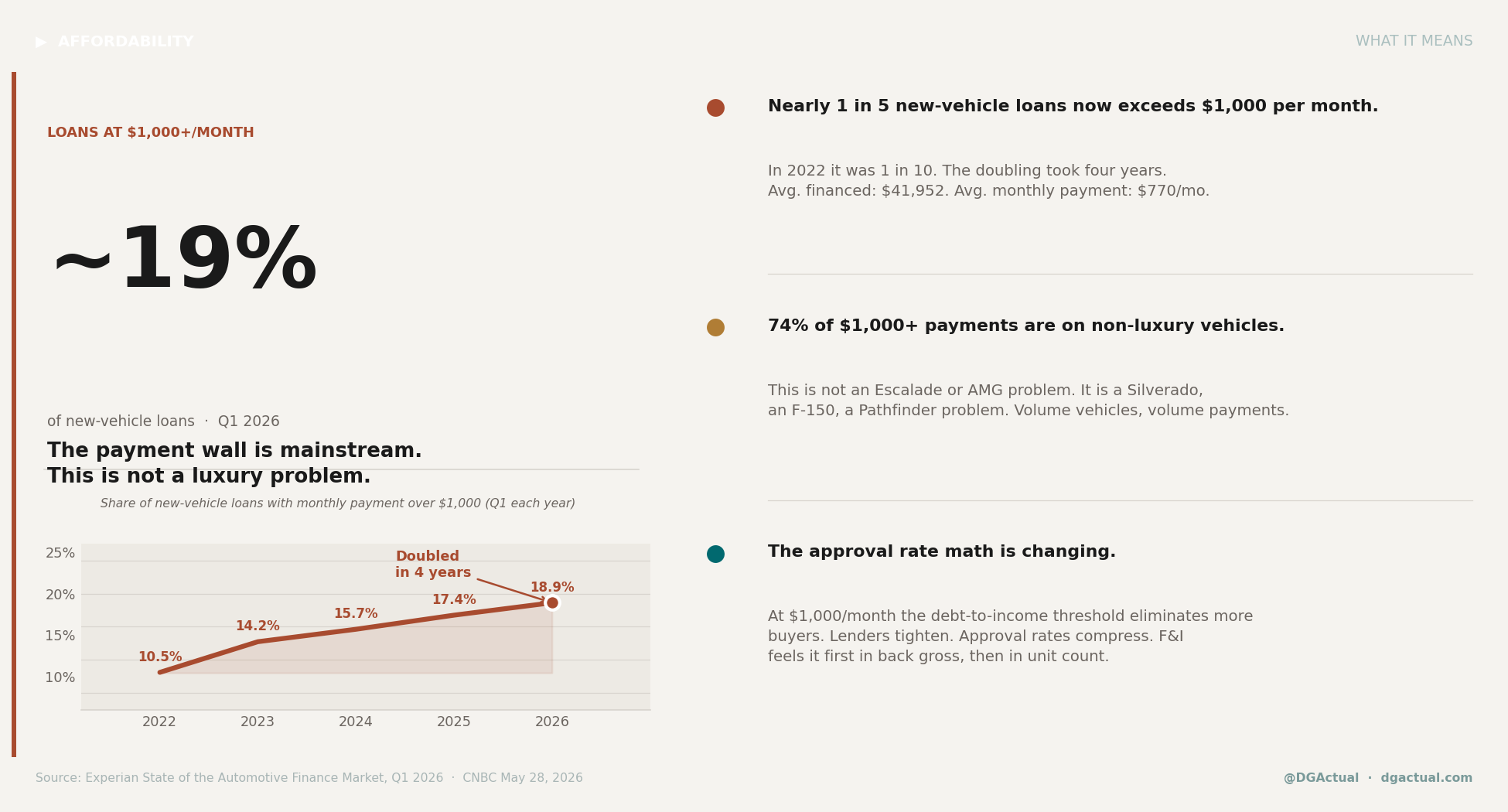

$1,000 a Month Is Now the Median Problem, Not the Outlier

Nearly 1 in 5 new-vehicle loans now exceeds $1,000 per month. In 2022 it was 1 in 10. That doubled in four years.

74% of those $1,000+ payments are on non-luxury vehicles. This isn't an Escalade problem or a Mercedes problem. It's a Silverado problem, an F-150 problem, a Pathfinder problem. Volume vehicles. Volume payments.

When the monthly payment clears $1,000, debt-to-income math starts eliminating buyers before they get to the pencil. Lenders tighten. Approval rates compress. Your F&I manager feels it first in back gross, then in unit count. The volume tier is where this lands hardest.

Total SAAR Says 16.3M. Retail Says 13.6M. Mind the Gap.

The headline SAAR number looks healthy. It isn't what you think.

Total SAAR includes fleet: rental, commercial, government. Fleet buyers pulled forward purchases ahead of tariff pricing in early 2026. Rental fleets restocked. Government contracts closed. Estimated retail SAAR for May: 13.6M. The gap between the headline and actual consumer demand is 2.7 million units.

Average incentive spend in May: $3,297. That's up from $3,050 in January 2025 — but still well below the ~$4,200 that supported similar retail SAAR in 2019.

The floor traffic you see in June is consumer demand. The fleet-inflated SAAR number is not. Build your Q3 floor plan around the 13.6M, not the 16.3M.

Used Prices Jumped $870 in a Single Month. Every Segment.

The CARFAX June Used Car Index published May 26 logged a $870 average increase in used-vehicle listing prices during May — a 3.1% gain in a single month, with every segment posting increases simultaneously. Hybrids and EVs led the surge at +$1,450 per unit. South region hybrid/EV used prices moved over $2,000 in one month.

New-vehicle average transaction prices at $49,025 are pushing buyers into used. Demand is meeting tightening supply and repricing fast.

If your used inventory was appraised three weeks ago, those book values are already behind retail. The dealers capturing maximum GPU this month are resetting appraisal standards weekly and tracking retail comps in real time, not at month-end. Hybrid and EV used inventory in particular should be repriced upward immediately.

Source: CARFAX Used Car Value Index, May 2026

419K Jeep Grand Cherokees Need a Software Update. Starting June 11.

NHTSA Recall 26V328 covers 419,035 Jeep Grand Cherokee (2022-2026 MY) and Grand Cherokee L (2023-2025 MY) SUVs for an Occupant Restraint Controller software flaw that may delay side airbag deployment in a crash. Remedy is a software update. Owner letters go out June 11 to 19.

No Do Not Drive advisory. But 419,000 units is a large, current, in-cycle population, most of them still inside the ownership window where trade-in conversations happen.

This is a service lane opportunity if you work it proactively. VIN-scan your market database against the recall population now. Outbound calls before the letters arrive puts your dealership first. Low-cost remedy, captive appointment, and a customer thinking about their car's reliability: that is the conversation that leads to the next vehicle purchase.

Source: NHTSA Recall 26V328 / Car and Driver

Credit Is Splitting Into Two Markets

TransUnion's Q1 2026 Credit Industry Insights Report puts hard data on something dealers are already seeing: the credit market is bifurcating. Super prime borrowers now represent 40.7% of all U.S. consumers, up from 36.9% in 2019. Subprime is growing too — up 100 basis points since 2019. The prime and near-prime middle is contracting.

Auto 90+ day borrower delinquency: 2.53%, up 10 basis points year over year. Non-prime consumers are carrying higher debt-to-income ratios and showing early performance stress.

Two F&I conversations are happening in the same showroom: the super-prime buyer who wants speed and transparency and will close fast, and the subprime buyer who needs creative deal structure and non-prime lender depth. Optimizing your process for only one of those lanes means leaving money on the table in the other.

Source: TransUnion Q1 2026 CIIR

DGActual Signal Intelligence covers the economic and market signals that move automotive retail. Published independently. No affiliate relationships with data providers.

Daniel Govaer · EVP Product, VINCUE · dgactual.com