Monday Signal Brief — June 23, 2026

The Fed isn't cutting. Credit stress is moving earlier. CarMax's finance arm just became the largest Tier 2 lender. Recalls, inventory, and one jobs number worth a callback. All of it in plain language.

A small thank you before we get into the data.

I have 25 DGActual merch packs going out this week — a mug and a die-cut sticker — to the first 25 subscribers who claim one. No purchase, no signup, no catch. I ship it to you, on me. This is just my way of saying thank you for reading every Monday.

Claim your free pack →US only. First come, first served. Ships via Printful. Your address is used only for shipping and is never stored or shared.

Here is what I am watching this week and what I would be doing about it at the desk.

The Fed isn't cutting. Stop waiting.

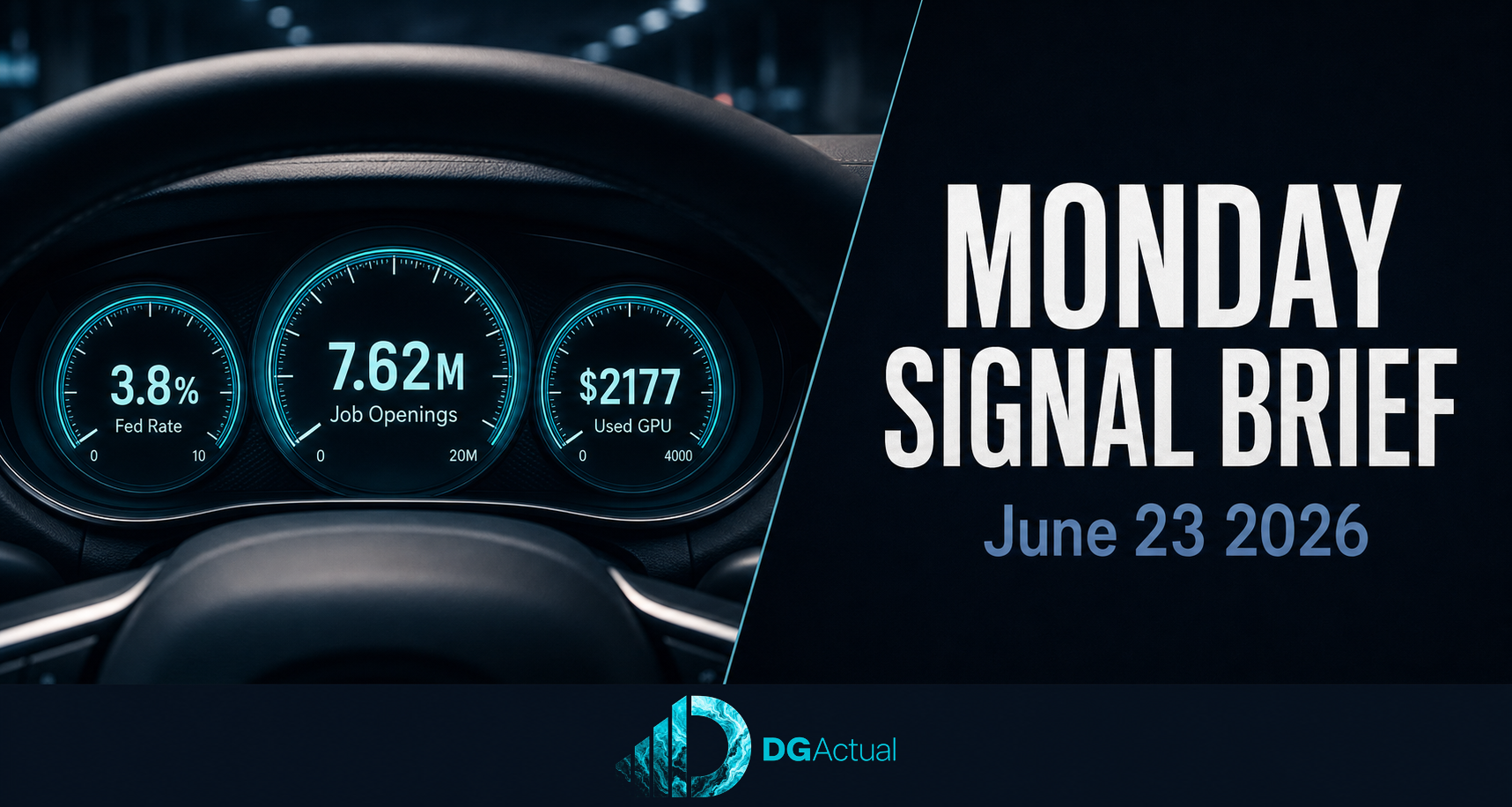

The Fed held rates at 3.5% to 3.75% last week. More importantly, the June projections moved up, not down. The median estimate for where rates land at year-end 2026 is now 3.8%. In March it was 3.4%.

That shift closes the door on the "rates will drop soon" story some managers are still telling themselves and their customers.

Auto loan rates price off the 10-year Treasury, not the Fed funds rate. A full one-point Fed cut translates to about $20 a month on a typical loan. OEM rate programs move the payment more than the Fed ever will.

What to do this week: Lean into leasing wherever the OEM program supports it. Payment is king right now, and a lease payment beats a financed payment on most popular vehicles. If you aren't actively presenting the lease option on every deal, you are leaving closes on the table. Also: if a customer walked your lot in the last 60 days and didn't buy because they were waiting on rates, call them back. The math is not getting better.

Your service drive is also a live pipeline. A customer who came in for an oil change last week is statistically closer to a purchase than a cold internet lead. If your BDC isn't touching service drive appointments for trade and purchase conversations, that is revenue sitting on the lot.

Credit is showing stress earlier than the headlines suggest

This one matters more than it sounds.

Auto loan performance data released last week showed a split. Prime borrowers are fine. Early-stage delinquencies in that group actually fell.

Non-prime borrowers are a different story. Payments are starting to break earlier in the loan cycle, not later. The 30 to 59 day bucket moved higher in May while the 60-plus day numbers improved. That sounds fine until you understand what it means: more people are beginning to miss payments, they just aren't deep enough yet for the headline rate to move.

When this pattern shows up in the ABS data, lenders respond before you feel it. Tighter conditions on certain paper. Slower approval turnarounds. More conditions on deals. You won't get an announcement. You'll just notice more friction.

This is a signal to run a clean book right now, while lenders are still moving normally.

CarMax: the story isn't the EPS beat. It's the finance arm.

CarMax posted a 39% EPS beat last week. Wall Street still sold the stock down 7% on earnings day.

Why? Because the more important number was what happened inside CarMax Auto Finance.

CAF is now the largest Tier 2 lender in the used vehicle market. In Q1, it absorbed market share that previously went to third-party Tier 2 lenders , the same lenders franchise dealers use every day. Third-party Tier 2 penetration at CarMax fell from 17.7% to 15.7% in one quarter.

That 2-point shift went directly into CAF. CarMax is building a captive finance ecosystem that makes the customer less likely to need outside lending and more loyal to the CarMax transaction.

For franchise dealers, the question worth asking is: if the Tier 2 lenders CarMax used to send business to are now losing share to a captive, does that change their pricing or appetite for your paper? It's worth a direct conversation with your finance relationships this week.

The used GPU number , $2,177, down $230 from a year ago , is also worth noting. CarMax is deliberately compressing its own front-end gross to drive volume. That is a competitive pricing posture at scale. The dealers who feel it are the ones competing on price rather than service, speed, and finance product.

Recalls your service lane needs to act on this week

Hyundai Palisade (2020–2025) , 568,576 units Side curtain airbags for third-row occupants may not deploy correctly in a crash. Campaign 26V034000. Not a Do Not Drive, but safety-critical. This is a large volume, family-oriented recall. If you have a Hyundai store, run your VIN list and start scheduling. Service capacity will fill fast once owner letters land.

Ford Focus (2012–2018) , 255,404 units Engine stall risk from a canister purge valve issue. A prior fix may not have been completed correctly on all vehicles. Campaign 26V369000. Good opportunity to bring owners in and bundle maintenance.

Jeep Wrangler and Gladiator (2021–2025) , If you covered this last week and haven't run your VIN list yet, do it today. The fire risk is real, the advisory is still active, and owner letters haven't landed yet. That window closes soon.

Chrysler Pacifica Plug-in Hybrid (2020–2022) , Same situation. Do Not Drive advisory still in effect. If you have one of these in service or on your lot, it needs to be addressed.

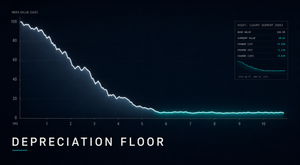

What your inventory is telling you right now

Fresh data as of this morning from 1.5 million active listings across 10 segments. This is Week 3 of the DARPI , the DGActual Retail Price Index , and for the first time this week we have three data points to compare.

Move it now: Minivans are turning in 66 days near-new. Near-new EVs are at 67 days. These are the two fastest-turning segments in the index, and this week EV volume is running 3% above the June baseline , the only segment where that is true.

The EV value story: near-new EV prices are at 99.6 on the index and value-tier EV prices are at 101.3 , the only segment in the index where value prices are above the June baseline. The near-new to value DOM spread is just 9 days (67 vs 76). That is historically tight. The depreciation floor is holding.

Watch the clock: Full-size trucks are sitting at 108 days near-new, luxury at 107 days. Value-tier trucks, luxury, and full-size cars and SUVs are all between 169 and 179 days. If those units have been on your lot 90-plus days, the conversation needs to move toward wholesale, not another price adjustment.

The full interactive dashboard , sortable by segment, DOM, price, and volume with three weeks of trend lines , is live at data.dgactual.com.

One number: 7.62 million

That is how many job openings the April JOLTS report showed, released June 2nd. The market expected 6.86 million. It beat by 750,000.

A strong job openings print means consumer confidence has a floor under it. The buyer who told you last month they were nervous about the economy now has less macro cover for waiting. If you have unsold shoppers from the past 30 to 60 days, this week is a legitimate reason to reach back out.

DGActual publishes every Monday morning.

Questions or feedback: reply to this email.