84-Month Auto Loans Are Almost As Common As New Leases

And growing at a faster rate. What it means for dealers.

[DEEP DIVE] Deal Structure / Consumer Finance

April 2026 · DGActual Signal Intelligence

The 84-Month Loan Just Became More Common Than a Lease. That Should Concern Every Dealer in America.

Sometime in the last 90 days, something crossed a line that has never been crossed before. The 84-month loan, a product we used to treat as a last resort, became more common at the desk than a 3-year lease. Not slightly more common. Statistically dominant. I have been in this business long enough to know that when a bad habit becomes a majority habit, the damage compounds quietly, and then arrives all at once.

The Numbers Are Not Subtle

Edmunds Q1 2026 data published April 2, 2026 shows 84-month or longer loans now represent 22.9% of all financed new vehicle purchases. An all-time high. In Q1 2019 that number was 13.4%. It was 21.2% just a year ago. The trajectory is not ambiguous. Meanwhile, Edmunds also reports the average amount financed hit a record $43,899 in Q1 2026, carrying an average APR of 6.9%, with only 2.6% of new vehicle loans at 0%. The average monthly payment sits at $773. Twenty percent of all financed deals now carry payments of $1,000 or more, up from 17.7% a year ago. The buyer is not getting relief from the longer term. They are getting a longer runway to the same cliff.

The Crossover Nobody Is Talking About

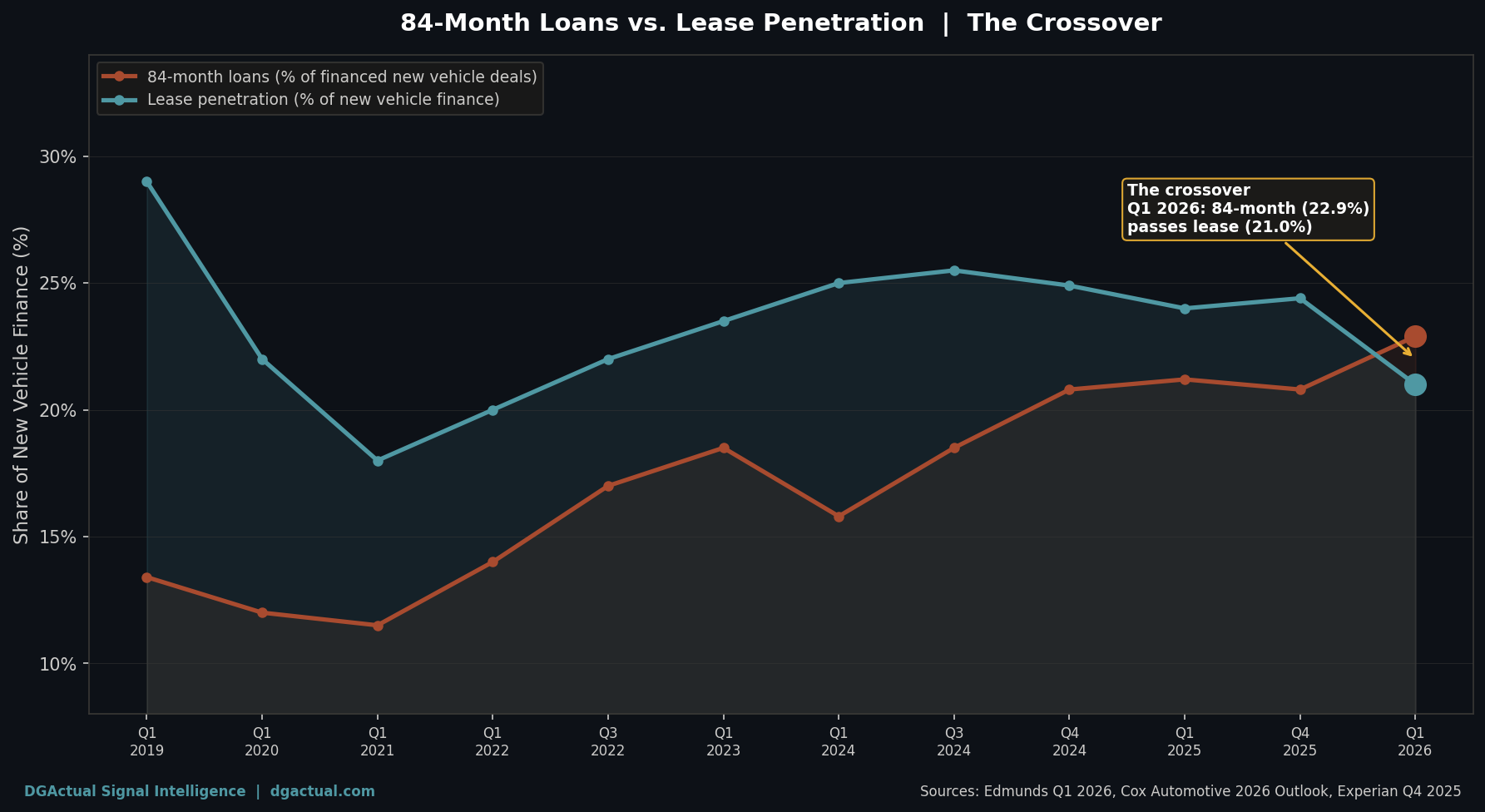

This is the number that stopped me. Cox Automotive's 2026 full-year forecast puts lease penetration at 21%. Experian's Q4 2025 data shows 24.37% of new vehicle finance transactions were leases. Either way you measure it, 84-month loans have now crossed or matched lease penetration. A 7-year loan is more common than a 3-year lease. That has never been true before. This is not because the lease became a bad product. Right now, the lease is arguably the best payment product on the floor. The crossover happened because we stopped presenting it. That is not a customer preference problem. That is a desk habit.

Leading indicator to watch: The AutoPayPlus dealer survey from March 27, 2026 has dealers already naming this the "84-month trade-in cliff." When these loans mature in 2028 and 2029, the negative equity problem they are generating right now compounds into something we do not have a product solution for.

The Math the Desk Is Not Running

Experian Q4 2025 puts the average new vehicle loan payment at $767/month and the average lease payment at $659/month. That is $108 per month cheaper on lease before a single OEM subvented program is applied. With subvented support in market right now, J.D. Power's March 2026 data puts the lease advantage at $120/month. Over 36 months, that is $3,888 in payment relief over the life of the deal. The buyer currently stretching to $916/month because they rolled negative equity into an 84-month loan, per Edmunds Q4 2025, could be sitting at $550 to $650 on a properly structured lease. Same vehicle. Different product. Completely different outcome for both of them, and for you.

Real Numbers. April 2026.

These are not projections. These are deals on the floor right now, per CarsDirect on April 5, 2026:

- F-150 Lightning: $249/month, 36 months

- Honda Prologue: $269/month, 36 months

- Hyundai IONIQ 9: $399/month, 36 months

- Kia EV9: $449/month, 36 months

These are mainstream vehicles at payments that would close deals currently dying at the desk. The OEM support is real. The programs are live. The question is whether the desk knows to present them before the customer hears the loan payment and walks.

The Compounding Problem

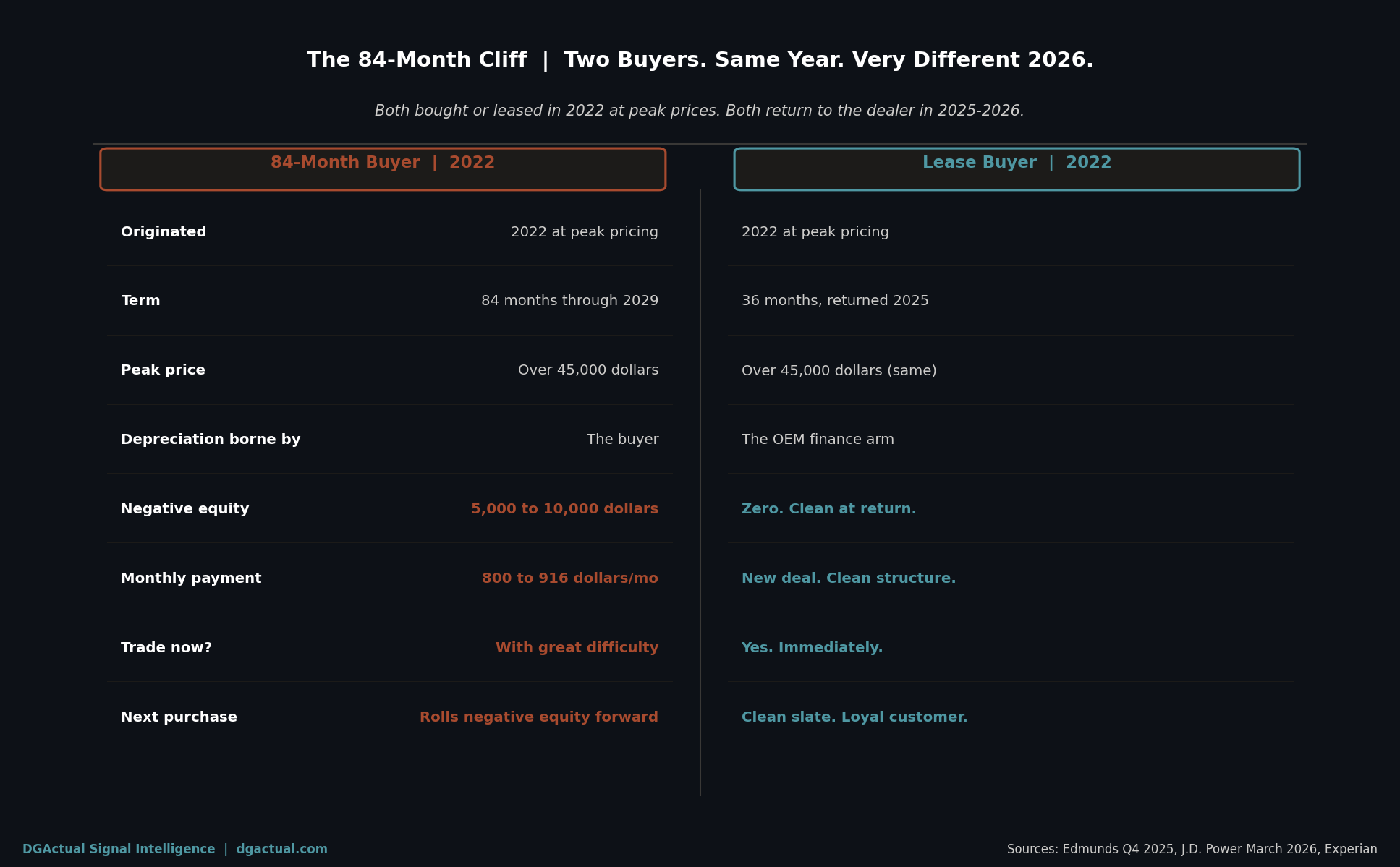

The 84-month buyer from 2022 is coming back. They are the 30.5% negative equity statistic J.D. Power reported in March 2026. They carry an average of $7,214 underwater, the highest Edmunds has ever recorded. You cannot solve that with another 84-month loan. But 40% of buyers rolling negative equity into a new deal are doing it on 84-month terms, according to Edmunds. They will be back in three years doing it again. This is how the cliff compounds: one generation of bad structure becomes the next generation's problem. CNBC covered this cycle in March 2026. The dealer who broke the cycle in 2022 with a lease has a customer walking back in 2025 clean, positive, ready to transact, with loyalty. The dealer who defaulted to 84 months has a customer walking back with $7,000 of your problem attached to them.

What the Lease Does That the Loan Cannot

At lease end, the negative equity is gone. No rollover. No cliff. The residual sits on the OEM's balance sheet, not on your customer's credit file. The buyer who leases in 2026 does not become the negative equity trade-in problem in 2029. They become a repeat customer on a clean deal. OEM programs right now are the strongest they have been in five years. Lease penetration has been declining while loan terms have been extending, which means the window of opportunity is open and there is competitive room to take it. It will not stay open. When rates compress and the market tightens again, the programs compress with them.

A Direct Ask

When the next payment-sensitive buyer walks in, show them the lease payment before the finance payment. Not instead of. Before. Let them see both with full information and make a real choice. The buyers who choose finance will close with better conviction because they compared and decided. The buyers who take the lease will be back in 36 months, clean, ready to go again. Both are good outcomes. The buyers who leave because the payment did not work, because we defaulted to a loan structure that put them at $800 a month when a lease would have been $550, those are the lost deals that never appear in the data but show up every month in the traffic that does not close. I have run stores. I have sat at the desk. I know what it feels like when the month goes wrong and you cannot identify why. Sometimes it is the product we did not present.

The structure we default to today is the customer we inherit tomorrow.

Daniel Govaer

EVP Product, VINCUE

Loyalty Project Manager, Beaver Toyota

Dealer Innovation Group Facilitator, MyKaarma

Former Award Winning Mercedes-Benz General Manager

NADA Academy Class N367 Graduate

Sources:

- Edmunds Q1 2026 finance data (April 2, 2026): https://www.autoremarketing.com/autofinjournal/records-set-in-edmunds-q1-data-reinforce-thought-of-cliff-connected-to-84-month-contracts/

- Edmunds Q1 2026 press release: https://www.edmunds.com/industry/press/average-amount-financed-for-new-vehicle-purchases-hits-record-43899-in-q1-2026-according-to-edmunds.html

- Cox Automotive 2026 outlook: https://www.coxautoinc.com/insights-hub/cox-automotive-2026-outlook/

- Experian Q4 2025: https://www.experianplc.com/newsroom/press-releases/2026/new-report-from-experian-automotive-highlights-growth-in-subprim

- J.D. Power March 2026: https://www.jdpower.com/business/press-releases/jd-power-globaldata-forecast-march-2026

- Edmunds Q4 2025 negative equity insights: https://www.edmunds.com/car-news/edmunds-q4-2025-insights-report.html

- CNBC negative equity March 2026: https://www.cnbc.com/2026/03/30/negative-equity-trade-ins-car-buyers.html

- AutoPayPlus 84-month cliff survey (March 27, 2026): https://www.autoremarketing.com/autofinjournal/records-set-in-edmunds-q1-data-reinforce-thought-of-cliff-connected-to-84-month-contracts/

- CarsDirect April 2026 lease deals: https://www.carsdirect.com/deals/electric